For years, payroll compliance in India operated through a layered system of separate labour laws, different wage definitions, overlapping registers, and state-level variations. That model has now changed.

India’s labour law reforms are intended to bring existing legislation under four separate codes with the aim of making things simpler for compliance, formalisation, better worker protections, and more consistency across industries.

For business leaders, the implication is clear:

Payroll is no longer a back-office function. It has become a strategic compliance function with direct impact on the following:

- Workforce cost structures

- Statutory liabilities

- Compensation design

- Employer risk exposure

- HR technology investments

- Audit readiness

TL;DR

- India’s labour law framework has shifted from 29 central labour laws to 4 consolidated Labour Codes.

- These 4 codes came into effect on 21 November 2025, and rules for implementation came into effect in 2026.

- Payroll is emerging as one of the most directly affected business functions due to changes in wage definitions, social security calculations, recordkeeping, and compliance processes.

- The revised wage structure has renewed focus on the widely discussed 50% wage composition principle, influencing PF, gratuity, and benefit calculations.

- Compliance is becoming increasingly digital, auditable, and integrated across HRMS and payroll systems.

The Four Labour Codes Every Business Leader Should Understand

The new labour codes are among the major changes in the labour policy in India in recent years. The aim is simplification, but the real-world implications run to the heart of payroll operations, employee benefits, compliance processes, and workforce governance.

| Labour Code | Primary Focus | Payroll Impact |

|---|---|---|

| Code on Wages, 2019 | Wage definition, minimum wages, bonus | Salary structure and payroll calculations |

| Code on Social Security, 2020 | PF, gratuity, social benefits | Employer contributions and deductions |

| Industrial Relations Code, 2020 | Employment relations and workforce management | Employment documentation and payroll workflows |

| Occupational Safety, Health and Working Conditions Code, 2020 | Working conditions and employment records | Attendance, leave, and, workforce tracking |

What Did the May 2026 Central Rules Actually Change?

This is the part most “labour codes explained” content still hasn’t caught up to. The Central Rules notified on 8 May 2026 cover wages, social security, dispute resolution, model standing orders, and working conditions across all four codes. A few specifics payroll and HR leaders should know:

- Floor wage mechanics are now defined. The centre will fix a national floor wage based on minimum living standards, food, clothing, housing, and other relevant factors, and states cannot set minimum wages below it.

- Appointment letters and health checks are mandatory. Employers must issue appointment letters to all workers and provide a free annual health checkup to employees aged 40 and above.

- Gig and platform workers now have a registration clock. Aggregators must register gig and platform workers on the designated portal within 45 days, a direct new compliance task for platform-economy employers.

- Creche provisions are now operational requirements, employers must provide creche facilities with CCTV, trained staff, and emergency arrangements for employees of either gender.

- ESI wage ceiling guidance is current: the Ministry has confirmed Rs 21,000 per month as the wage ceiling for ESI coverage at present.

- Coverage isn’t uniform yet. The central rules apply where the central government is the appropriate authority, broadly central PSUs, banking, insurance, telecom, mining, and similar sectors. While most other employers will be governed by state rules, many of which are still in draft. If you operate across states, this is the detail your legal team needs to confirm first.

How Does the New Wage Definition Change Payroll Economics?

The standardisation of “wages” remains the single most consequential change for payroll math.

Historically, compensation structures leaned on allowances with comparatively low basic pay. Many companies structured salaries with basic pay as low as 30–40% of total compensation specifically to minimise statutory outlays. That’s no longer compliant. Under the notified rules, wages, basic pay, DA, and retaining allowance must equal at least 50% of total remuneration, and any excess in excluded allowances above that threshold gets added back into the statutory wage base for benefit calculations.

What this will affect:

- Contribution into the Provident Fund

- Gratuity obligations, like last-drawn basic pay, typically rise, increasing payout

- Calculating leave encashment

- Overtime payments

- Notice pay calculations

- Long-term employee benefit liabilities

| Earlier Structure | Current Structure Trend |

|---|---|

| Lower basic + higher allowances | Higher wage-linked component |

| Lower statutory outflow | Higher statutory obligations |

| Higher immediate take-home | Potential shift toward long-term benefits |

This is why many organisations are revisiting CTC design proactively rather than waiting for an audit to force the issue. Restructuring after the fact is more disruptive than building compliant structures into new offers and renewals now.

Payroll Compliance Is Becoming More Visible

The new system combines simplicity with accountability. Having auditable payroll systems is no longer an option. The requirements have become the following:

- Digitized records for all employees centrally

- Timely wage payments with timestamped evidence

- Trackable approvals processes

- A consistent salary nomenclature system throughout the organization

- Documentation for compliance purposes available for inspection, not compiled at the last minute on receiving notice

For CHROs and CFOs, this means payroll accuracy has become part of governance, not just administration.

How Will Social Security Compliance Change for Employers?

The Code on Social Security extends well beyond traditional payroll deductions. It explicitly extends social security benefits to gig workers, platform workers, and unorganised sector employees, categories that were largely outside formal coverage before.

Payroll leaders should evaluate:

- After basic pay is recalculated under the new wage definition, evaluate the PF impact

- Gratuity accounting changes from a higher wage base

- Consistency of benefit calculations across business units

- Controls on worker classification (employee vs. contractor vs. fixed-term)

- Gig/platform worker registration timelines, where applicable

Questions for leaders to ask themselves:

- Is there agreement between payroll and HR data on a line-by-line basis?

- Can we automate our statutory calculations, or do they have to be recalculated each time?

- Are our current payroll reporting processes able to withstand scrutiny?

- Are our reward models designed to work with the legislation as notified, not as drafted by the end of 2025?

Salary Structures May Need Redesign, Not Just Adjustment

The most common mistake is misinterpreting the labour codes as a payroll configuration issue. It is much broader than that. These codes basically incorporate:

- Compensation Strategy – which salary structure, variable compensation design, benefit strategy

- Financial Planning – employer contributions projection, budget modelling, cost per employee

- Workforce Governance – employment documentation, filing policy, consistency of policy among units

Organisations that model the cost impact ahead of their next compensation cycle have a much smoother transition than those reacting mid-cycle.

Multi-State Employers Face an Uneven Compliance Map

The codes aim for national uniformity, but real-world rollout still runs through state implementation. Several states are yet to finalise their own rules, even with the central framework now settled. Organisations operating across states should prioritise the following:

- Regulation tracking at the state level, rather than an isolated review

- Coordination of policy between business units

- Payroll governance centrally controlled but flexible in local compliance

- Review cycle based on notification of state changes throughout 2026

This matters most for large, manpower-intensive, and geographically dispersed workforces. Exactly the profile where a manual, region-by-region tracking process breaks down fastest.

HR Technology and Payroll Automation Are Becoming Compliance Infrastructure

In 2026, payroll systems function as compliance engines, not just processing payroll. This change now encompasses:

- Automated statutory calculations based on the notified definition of wages

- Compliance warnings generated from the updates to the state’s laws

- Digitized audit trails

- Integrated employee information for both HR and payroll

- Payroll validation based on the current law rather than the law that was in effect six months ago

The situation after May 2026 favours openness. Not only is manual reconciliation less efficient, it poses a 100% compliance risk.

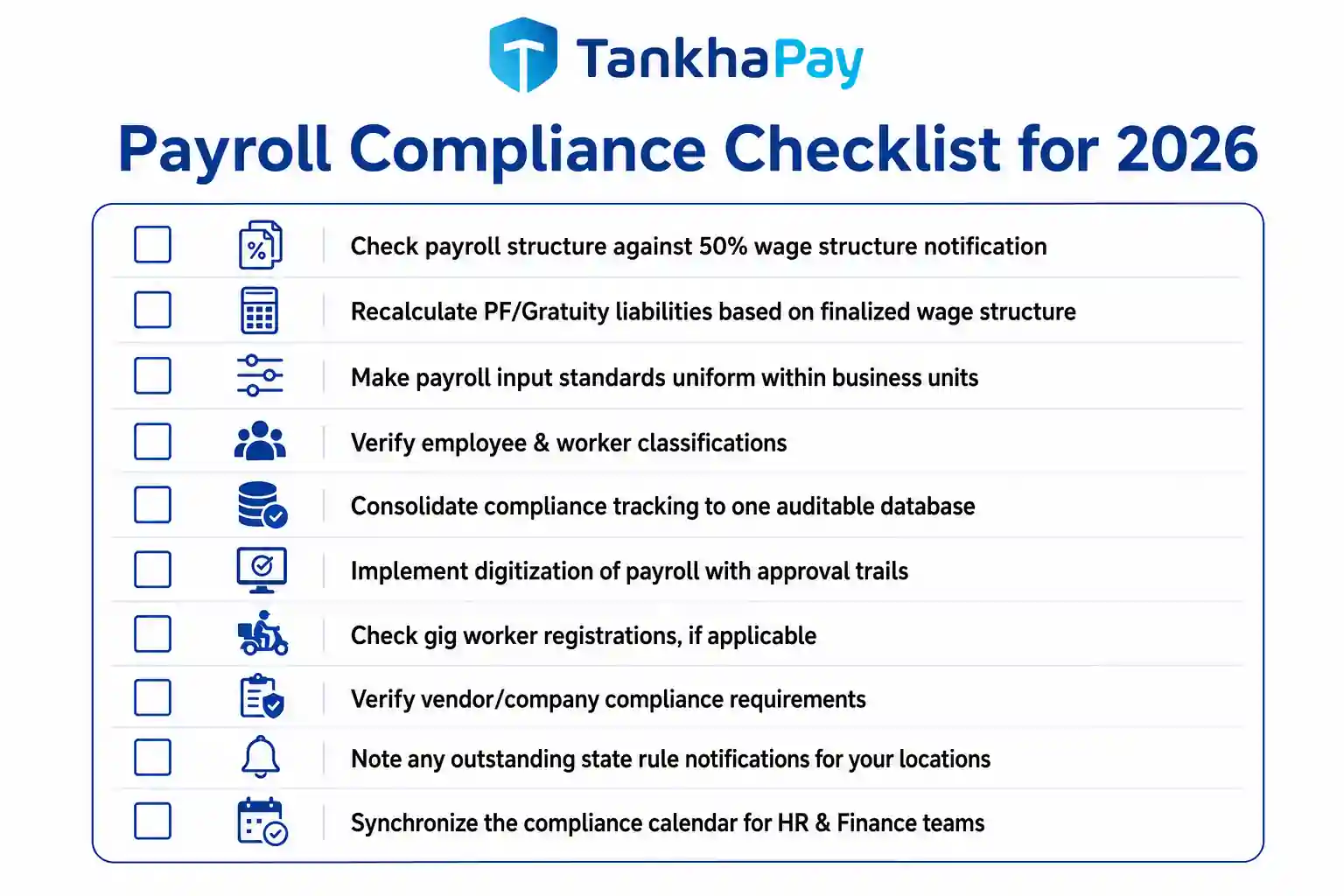

Payroll Compliance Checklist for 2026

☐ Check payroll structure against 50% wage structure notification

☐ Recalculate PF/Gratuity liabilities based on finalized wage structure

☐ Make payroll input standards uniform within business units

☐ Verify employee & worker classifications

☐ Consolidate compliance tracking to one auditable database

☐ Implement digitization of payroll with approval trails

☐ Check gig worker registrations, if applicable

☐ Verify vendor/company compliance requirements

☐ Note any outstanding state rule notifications for your locations

☐ Synchronize the compliance calendar for HR & Finance teams

Final Thoughts

The labour codes of India have never been limited to mere regulatory consolidation. As the Central Rules have been notified by May 2026, the time for “upcoming reform” has ended, and the “operating reality” is here. The difference between those who prepared and those who did not will soon be seen in the coming audit.

The issue for CEOs, CHROs, and CXOs is not whether labor law reform impacts payroll but whether your payroll systems, compensation models, and compliance process have been designed according to current legislation and not based on the draft legislation which your organization reviewed last year.

That’s the gap that TankhaPay is built to close, transforming the statutory wage calculation system, register, and audit trail into something more updated to the laws than in need of being caught up to.

FAQs

Do the new labour codes increase payroll costs?

Possibly, but it all depends on what kind of salary structure you already have. Companies that have an allowance-based compensation system will probably feel a greater need to pay increased statutory contributions because of the 50% rule now becoming a notified rule.

Will employee take-home salary reduce?

Not in all cases. The results will be determined by how the individual organizations make adjustments to CTC due to such changes.

Are the Central Rules now final everywhere in India?

Yes, from the central perspective, the Central Rules have been notified through gazette notification dated 8 May 2026. However, it is relevant only where the government is the “appropriate authority” for the particular organization. Some states still do not have their rules in place.

Are labour codes only an HR responsibility?

No. Payroll compliance now intersects HR, finance, legal, operations, and executive governance.

Should businesses act now or wait for more state-level clarity?

Move forward with what is definite (definition of wages, duties at the central level) and implement a system to track developments that are being implemented in states. Waiting for complete uniformity in the country before taking action is not an option anymore.

: 16 Companies Scored on Compliance")

: Differences, Costs & Which Hiring Model Is Right for Your Company?")

: Cost, Compliance & Decision Framework for Hiring in India")