Key Takeaways

- Audit your wage definition against the Code on Wages interpretation; the most optimised CTC structures may face upward revision in PF/ESI liability.

- Map your multi-state compliance obligations – PT and LWF registrations are often the first casualties of rapid geographic expansion.

- Review contractor classification rigorously – the ESIC and EPF coverage expansion under the new codes make this a significant risk area.

- Establish board-level visibility on payroll compliance status, not just HR-level reporting.

- Invest in a compliance calendar system – system-driven deadline tracking reduces the single largest cause of default, which is missed timelines.

Payroll compliance penalties in India usually take center stage when employers fail to comply with statutory obligations such as EPF contributions, ESI payments, TDS deductions, gratuity payments, professional tax filings, or wage payment rules. Penalties may include interest charges, financial damages, prosecution, and, in certain cases, imprisonment of responsible company officers.

Why Payroll Compliance Failures Are a Board-Level Risk in 2026?

India’s regulatory environment around employment and wages has never been more consequential. With the Central Government’s push to consolidate 40+ labour laws into 4 Labour Codes, i.e., the Code on Wages (2019), the Industrial Relations Code (2020), the Code on Social Security (2020), and the Occupational Safety Code (2020). Currently, the payroll compliance framework in India is undergoing the most significant structural change in seven decades.

But no complexity has disappeared. States are adopting these codes at different rates. New requirements for compliance are being added to legacy obligations that remain in effect until notification at the state level is complete. This is not a back-office issue for CEOs and CHROs – it’s a business continuity, reputational, and financial risk.

Think of the ripple effect of a single payroll compliance failure:

- Immediate monetary penalties on contributions, wages, or reports

- Compound interest and damages accumulating month over month

- Liability of directors and designated officers for criminal acts

- Regulatory scrutiny leading to wider audits of all statutory obligations

- Erosion of employee trust impacts retention and employer brand

What Is India’s Payroll Compliance Framework?

India’s payroll statutory framework involves multi-statute, multi-agency compliance. This means that employers have to be compliant with the requirements of federal statutes, as well as state-level modifications and industry-level statutes.

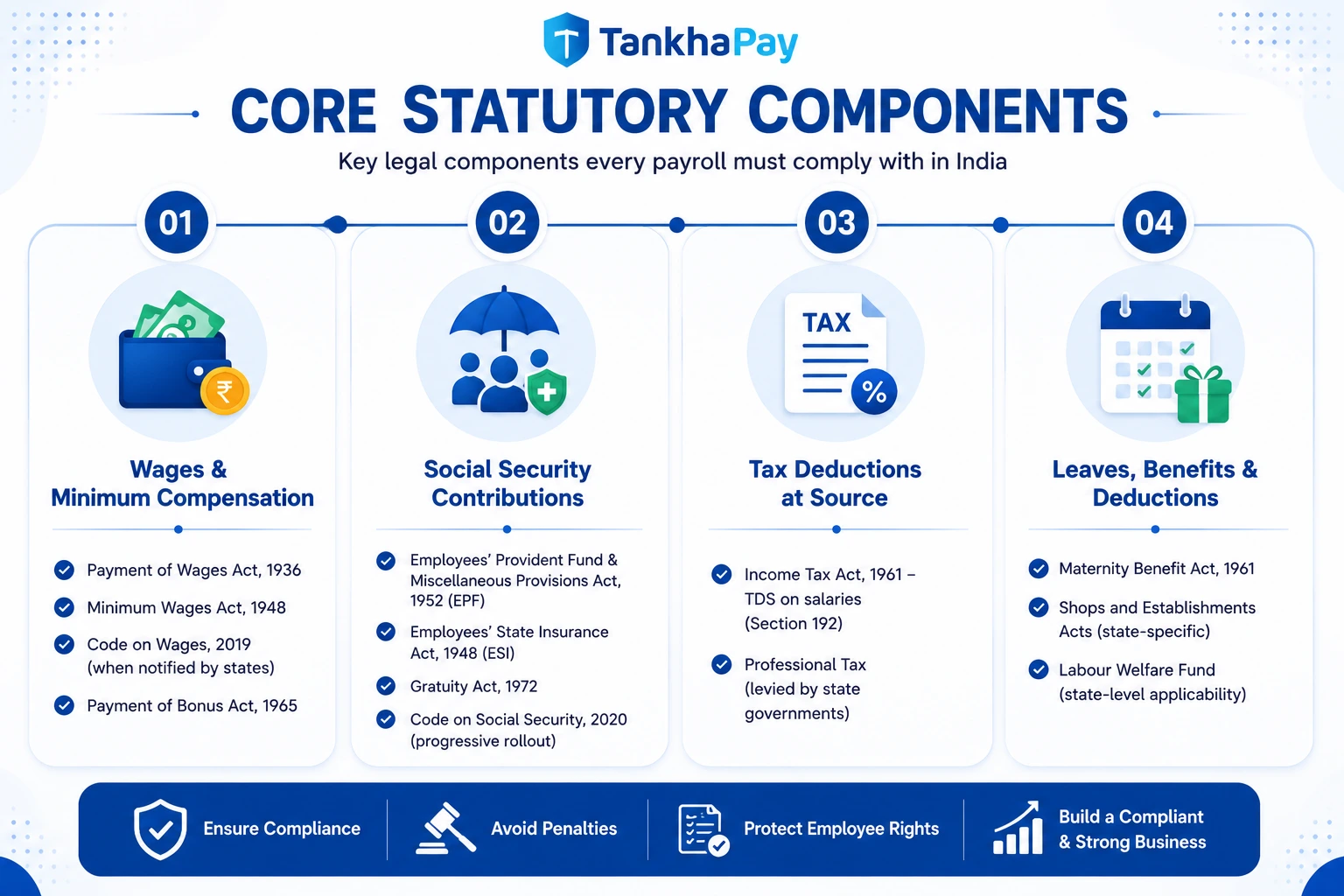

Core Statutory Components

1. Wages & Minimum Compensation

- Payment of Wages Act, 1936

- Minimum Wages Act, 1948

- Code on Wages, 2019 (when notified by states)

- Payment of Bonus Act, 1965

2. Social Security Contributions

- Employees’ Provident Fund & Miscellaneous Provisions Act, 1952 (EPF)

- Employees’ State Insurance Act, 1948 (ESI)

- Gratuity Act, 1972

- Code on Social Security, 2020 (progressive rollout)

3. Tax Deductions at Source

- Income Tax Act, 1961 – TDS on salaries (Section 192)

- Professional Tax (levied by state governments)

4. Leaves, Benefits & Deductions

- Maternity Benefit Act, 1961

- Shops and Establishments Acts (state-specific)

- Labour Welfare Fund (state-level applicability)

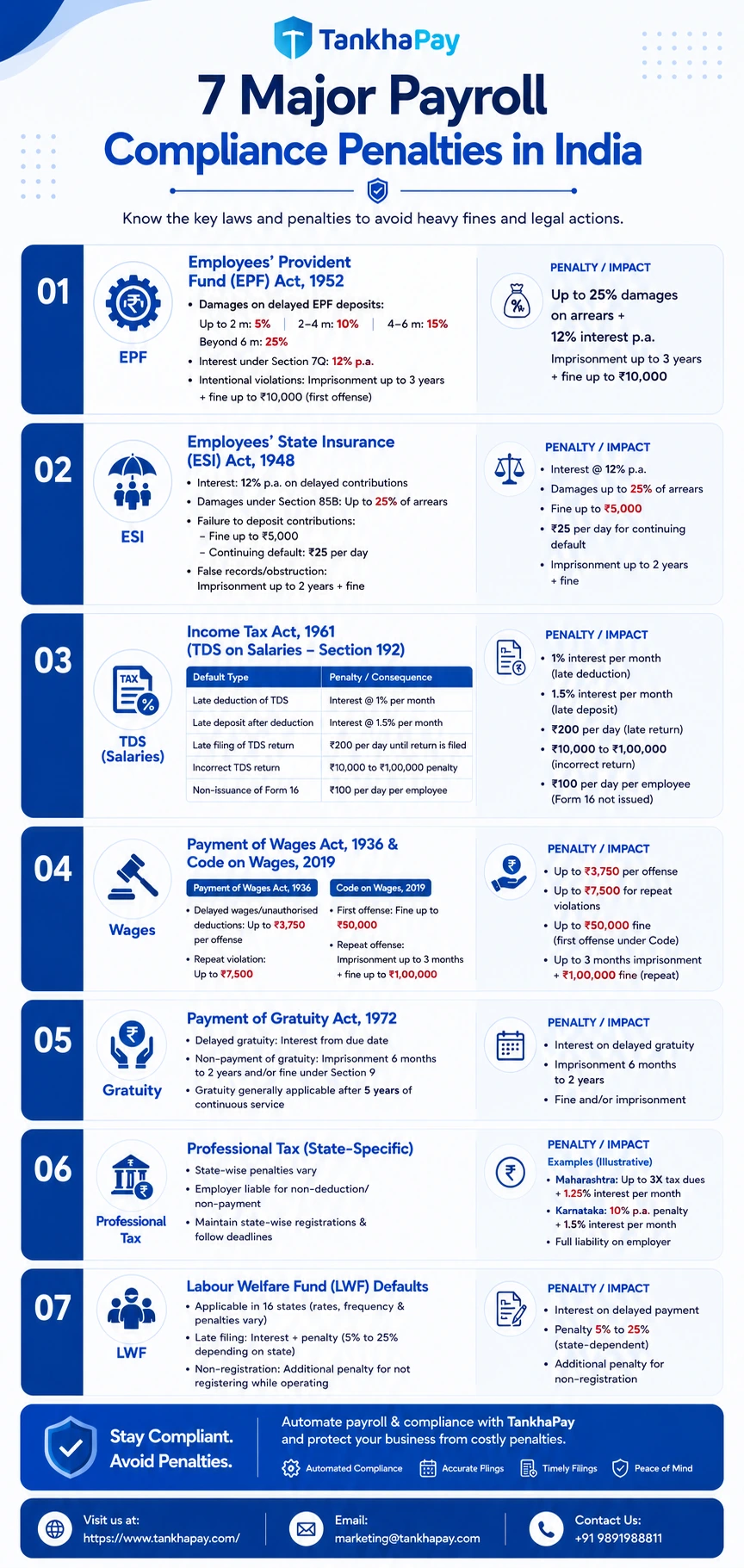

The 7 Major Payroll Compliance Penalties in India

Major payroll compliance penalties in India need to be understood thoroughly. Below is the structured format of the same.

Penalty 1 – Employees’ Provident Fund (EPF) Act, 1952

EPF non-compliance is among the most common and costly exposures for Indian employers.

Default in deposit of contributions:

- Damages under Section 14B: EPFO revised the rate of damages payable by employers for delayed remittance of EPF, EPS, and EDLI contributions. Since June 2024, damages have been generally levied at 1% per month of the arrears amount, subject to applicable EPFO provisions and notifications. In addition to damages, employers remain liable to pay interest under Section 7Q on delayed contributions.

-

- Up to 2 months: 5%

- 2–4 months: 10%

- 4–6 months: 15%

- Beyond 6 months: 25%

Interest under Section 7Q:

- Simple interest at 12% per annum on delayed contributions.

Criminal Penalty under Section 14:

- Intentional false filing or any violations can lead to punishable imprisonment up to 3 years, plus a fine up to ₹10,000 (for the first offense) and up to 5 years & ₹25,000 for repeated defaults.

EDLI (Employees’ Deposit Linked Insurance) default:

- Treated equivalently to EPF default for penalty purposes.

Under the EPF Act, the employer bears 100% responsibility for both the employer and employee shares in case of non-deposit. Courts have consistently held that deducting but not depositing employee contributions is treated as a more serious offense.

Penalty 2 – Employees’ State Insurance (ESI) Act, 1948

Delayed or non-payment of contributions:

- Simple interest at 12% per annum on outstanding amounts.

- Damages under Section 85B: Up to 25% of arrears (discretion of ESIC authorities).

Criminal liability under Section 85:

- Failure to deposit payments: Fines up to ₹5,000 and continued failure to make payments charges up to ₹25 per day as a continuing default fine.

- Obstructing an inspector or making a false entry: Imprisonment for up to 2 years and a fine.

Coverage threshold (2026):

- Establishments with 10 or more employees and wages up to ₹21,000/month (₹25,000 for persons with disabilities).

Penalty 3 – Income Tax Act, 1961 (TDS on Salaries – Section 192)

TDS default under payroll is governed by multiple provisions of the Income Tax Act:

| Default Type | Penalty Provision | Consequence |

|---|---|---|

| Non-deduction of TDS | Section 201 | Employer treated as “assessee in default”; liable for the full tax + interest |

| Late deduction | Section 201(1A) | Interest @ 1% per month from date of payment to date of deduction |

| Late deposit after deduction | Section 201(1A) | Interest @ 1.5% per month from date of deduction to actual deposit |

| Non-filing/late filing of TDS returns | Section 234E | ₹200 per day until return is filed (subject to TDS amount) |

| Incorrect TDS return | Section 271H | Penalty ₹10,000 to ₹1,00,000 |

| Non-issuance of Form 16 | Section 272A | ₹100 per day per employee |

The Income Tax Department’s centralised processing of TDS statements means discrepancies between Form 26AS and employer filings are automatically flagged – making clean payroll data a first line of defense.

Penalty 4 – Payment of Wages Act, 1936 & Code on Wages, 2019

Classic Act violations:

- Unauthorised deductions or delayed wage payment: Fine up to ₹3,750 per offense (revised under the Payment of Wages (Amendment) Act, 2017).

- Repeat violations: Fine up to ₹7,500.

Under the Code on Wages (where notified):

- Late payment of wages: Fine up to ₹50,000 for a first offense.

- Repeat offenses: Imprisonment up to 3 months + fine up to ₹100,000.

The Code on Wages also introduces the concept of a floor wage; it is a national minimum below which no state minimum wage can be set. Non-compliance with minimum wage obligations triggers both financial and criminal liability.

Penalty 5 – Payment of Gratuity Act, 1972

Employer defaults:

- Failure to pay gratuity on time after it becomes payable: Simple interest at the applicable rate from the due date.

- Non-payment of gratuity: Under Section 9 of the Payment of Gratuity Act, employers who fail to comply with the Act may face imprisonment, fines, or both.

- The offense relates specifically to non-payment of gratuity, the employer may be punished with imprisonment of not less than 6 months and up to 2 years, unless the court records reasons for imposing a lesser punishment. Interest may also become payable on delayed gratuity payments.

Critical trigger: Gratuity is paid after 5 years of continuous service with the same employer. However, some court decisions have ruled that 4 years and 240 days of continuous service are sufficient in some circumstances, but employers should seek legal advice before relying on this interpretation, as its applicability depends on the facts and the judicial precedent.

Penalty 6 – Professional Tax (State-Specific)

Professional Tax is a state-level collection of taxes applicable in approximately 21 states and UTs, including Maharashtra, Karnataka, West Bengal, Tamil Nadu, Andhra Pradesh, Telangana, Gujarat, and others.

Non-compliance consequences (illustrative – vary by state):

- Maharashtra: Have a penalty up to 3 times the tax dues, plus interest at 1.25% per month.

- Karnataka: Impose a penalty of 10% of unpaid tax per annum plus interest at 1.5% per month.

- Failure to deduct from employees and deposit: Employer bears full liability.

Multi-state employers must maintain state-wise professional tax registrations and adhere to separate filing calendars for each state.

Penalty 7 – Labour Welfare Fund (LWF) Defaults

The Labour Welfare Fund, or LWF, applies in 16 different Indian states, with contribution amounts, frequencies (monthly/half-yearly/annual), and penalties varying significantly.

Common penalty structure:

- Late filing: Simple interest along with a penalty (ranging between 5 and 5–25% based on the state).

- Non-registration: An additional penalty for not registering while operating.

Why Is Payroll Compliance Failure Exponentially Costly?

A key insight that C-suite leaders must incorporate: the major payroll compliance penalty in India is not a one-time cost. They compound.

Illustrative Scenario (100-employee company, 6 months of EPF default)

| Component | Calculation | Amount |

|---|---|---|

| Total EPF dues (arrears) | ₹5,00,000 | ₹5,00,000 |

| Damages @ 25% (>6 months) | 25% of ₹5,00,000 | ₹1,25,000 |

| Interest @ 12% p.a. (6 months) | ₹5,00,000 × 6% | ₹30,000 |

| Total liability | — | ₹6,55,000 |

The above-discussed components don’t include legal costs, potential criminal charges against board members, or reputation-related issues when raising funds, conducting due diligence for M&A transactions, or pursuing government tenders.

New Compliance Requirements Under the 4 Labour Codes

India’s shift to the 4 Labour Codes is one of the defining regulatory developments of this era. As of mid-2026:

- Central rules have been notified for all 4 codes.

- Employers working across different Indian states should continue to monitor state-specific implementation and payroll compliance requirements in India because operational readiness and state-level rule adoption may continue to change.

- Legacy acts continue to apply in states yet to notify.

Key New Compliance Requirements Employers Must Prepare For:

- Unified Definition of “Wages” (Code on Wages) The Code introduces a definition of wages where exclusions such as HRA, conveyance, and other allowances do not exceed 50% of the total compensation. This will affect the calculation of PF contributions, since some companies may have been organised in a way to minimise PF contributions.

- Expanded Gratuity Coverage (Social Security Code) Applicability is extended to fixed-term employees on a pro-rata basis, and there’s no minimum tenure threshold for FTEs.

- ESIC Expansion Social Security Code enables ESIC coverage to be extended to all districts and potentially to gig and platform workers, which helps in creating new payroll compliance obligations for companies relying on a contract/gig workforce.

- Changed Calculation Basis for PF Under the Code on Social Security, contributions must be calculated on the new wage definition, removing the engineering common exemption under legacy structures.

- Compliance Return Unification A single combined annual return is envisioned under the Labour Codes – but until states fully notify, employers must continue dual compliance.

In Brief: What are the new payroll compliance requirements under India’s Labour Codes?

Major changes incorporate a single definition of wages that impacts PF/ESI calculation, pro-rata gratuity for contractual or temporary employees, expanded ESIC coverage, and a combined annual return filing. But the implementation of these new compliances can vary by state as of 2026

What Best-in-Class Payroll Compliance Looks Like?

Here is how CXOs and CHROs can assess the maturity level of their payroll compliance process:

Monthly Payroll Compliance Checklist

Pre-Payroll (by 20th of month):

- Check employee entry, exit, and changes in payroll system

- Compare attendance, leaves, and overtime details

- [Confirm minimum wages applicable state-wise/categorically

- Check if tax deduction calculation is working as per the annual salary projections

Processing:

- Do gross-to-net calculations with all mandatory deductions

- Create EPF ECR (Electronic Challan cum Return)

- Create ESI challan

- Calculate Professional Tax based on respective slabs of individual states

Post-Payroll (Deposit Deadlines):

| Statutory | Deposit Deadline | Filing Deadline |

|---|---|---|

| EPF (employer + employee) | 15th of the following month | Monthly ECR |

| ESI | 21st of the following month | Half-yearly return (May 11, Nov 11) |

| TDS (non-government) | 7th of the following month (Mar: 30th April) | Quarterly – Q1: Jul 31, Q2: Oct 31, Q3: Jan 31, Q4: May 31 |

| Professional Tax | Varies by state | Monthly/quarterly/annual |

| Labour Welfare Fund | Varies by state | Half-yearly/annual |

What Are the Biggest Payroll Compliance Risks for Your Business?

Different business profiles face different risk concentrations in India’s payroll compliance framework:

| Business type | Highest Risk Areas | Why |

|---|---|---|

| Startup (< 50 employees) | TDS defaults, PF registration delays | Lean finance teams, rapid headcount growth |

| IT/ITeS (> 200 employees) | Wage definition, PF computation | Complex CTC structures; variable pay |

| Manufacturing | ESI, Minimum Wages, LWF | Blue-collar workforce; multi-shift payroll |

| Multi-state employer | Professional Tax, LWF | State-specific rules; decentralised HR |

| A company with gig workforce | ESI (new), Social Security Code | Expanding scope under new Codes |

| MNC India subsidiary | TDS, FEMA interaction | Expat payroll; equity-linked compensation |

Also Read: What is Multi-Country Payroll? Solutions & Compliance Tips

How Can Payroll Compliance Failures Impact Directors and Senior Executives?

One aspect significantly underweighted in boardroom discussions is personal liability. Most payroll statutes in India have provisions that pierce the corporate veil:

- EPF Act, Section 14A: Where an employer is a company, every person responsible for the conduct of the business at the time of the default can be held liable, including directors and designated HR/finance heads.

- ESI Act, Section 85: Similarly imposes personal criminal liability on persons in charge.

- Income Tax Act, Section 278B: Officers in charge of the company are deemed personally guilty for TDS offenses unless they prove due diligence.

This means that non-compliance is not just a company-level financial exposure; it is a personal legal risk for the CHRO, CFO, and designated compliance officer.

Red Flags That Signal Systemic Payroll Compliance Risk

The following warnings should be treated as early-warning indicators by CHROs and internal audit teams:

- Challan vs. payslip mismatches – EPF/ESI contributions are deducted from employees, but deposited amounts differ from payroll registers.

- Delayed month-end closes – Finance teams routinely closing payroll after the 15th of the following month create structural EPF default risk.

- Informal contractor classification – Workers deployed as “contractors” who functionally meet the definition of employees under the EPF/ESI Acts.

- Legacy salary structures – CTCs built to minimize statutory deductions may no longer hold under the Code on Wages’ wage definition.

- State multiplicity gaps – Multi-state employers without location-specific PT or LWF registrations.

- No unified compliance calendar – Teams are relying on email reminders rather than a system-driven compliance calendar.

- Absence of a compliance register – Statutory requirements under the Shops & Establishments Act and Factory Act to maintain registers that are either not maintained or outdated.

FAQ

Can an employer be imprisoned for payroll non-compliance in India?

Yes, according to the EPF, ESI, and Code on Wages Act, the employer shall be liable for imprisonment ranging from six months to five years for any type of wilful default or obstruction to the proceedings.

Does the new Code on Wages apply across all of India in 2026?

Yes, however, it is a matter of discretion for individual states to implement it. Up until mid-2026, only some states have implemented the code, while most other states are still at various stages of implementation of this law. Until that time, old laws will prevail where individual states do not introduce new rules.

What is the penalty for not filing TDS returns on time?

The delay in filing of returns is penalised under Section 234E of the Income Tax Act with a daily charge of ₹200 till the return filing, capped at the maximum amount of the total TDS. Other penalties are applicable under Section 271H between ₹10,000 and ₹100,000.

Is Professional Tax applicable to all Indian employees?

No. Professional Tax is a state-level levy and applies only in states that have enacted PT legislation, approximately 21 states and UTs. The maximum PT that any state can levy is ₹2,500 per year per employee (under Article 276 of the Constitution).

Payroll compliance is not just an HR issue anymore – it’s a business risk that affects financials, governance, and even reputation. TankhaPay helps organizations in streamlining payroll processes, ensuring statutory compliance, and maintaining audit-proof documentation without any issues. By automating compliance tracking, companies can mitigate risks of fines, interest, and legal hassle.

: 16 Companies Scored on Compliance")

: Differences, Costs & Which Hiring Model Is Right for Your Company?")

: Cost, Compliance & Decision Framework for Hiring in India")